Cláusula de Alcance en aviación regional

AW | 2017 10 10 12:44 | INDUSTRY / AIRLINES MARKET

Embraer y Mitsubishi no podrían expandir sus ventas a Estados Unidos por las «Cláusula de Alcance» para las aeronaves Embraer E175-E2 y Mitsubishi MRJ-90

Los pilotos de las principales aerolíneas esperan mantener las reglas vigentes en su nuevo contrato de trabajo que impiden que la aerolínea estadounidense vuelen aviones por encima de un cierto peso en rutas regionales. Esto representa un golpe a Embraer S.A. y Mitsubishi Heavy Industries Ltd., cuyos últimos modelos superan ese límite, imposibilitando las ventas en el mercado estadounidense, como aeronaves regionales.

El nuevo contrato de trabajo de los pilotos mantendrá lo que se conoce como una «Cláusula de Alcance», que restringe aviones de más de 86.000 libras y con más de 76 asientos en rutas regionales. Los resultados de la votación sobre el nuevo contrato se esperan el 1 de diciembre 2017.

La cláusula protege efectivamente puestos de trabajo piloto bien remunerados en las principales aerolíneas, ya que impide a la compañía utilizar aviones más grandes en rutas regionales subcontratadas, que generalmente pagan menos y tienen condiciones de trabajo inferiores.

Embraer & Mitsubishi pelean el mercado EEUU

Cuando la ingieniería de Embraer y Mitsubishi diseñaron sus últimos aviones regionales, con motores más pesados pero más eficientes, esperaban que la cláusula de alcance se hubiera cancelado, pero los sindicatos han logrado mantenerla.

El voto de Delta seguirá las decisiones similares de los sindicatos de American Airlines Group Inc. y United Continental Holdings Inc. a principios de este año como en 2015. La oposición de los pilotos a las cláusulas de alcance es un problema para la aeronave regional Embraer E175-E2 que se entregará en 2020 y el avión Mitsubishi MRJ90, programado para entrega a mediados de 2018, que exceden ambos el límite de peso.

El voto de Delta seguirá las decisiones similares de los sindicatos de American Airlines Group Inc. y United Continental Holdings Inc. a principios de este año como en 2015. La oposición de los pilotos a las cláusulas de alcance es un problema para la aeronave regional Embraer E175-E2 que se entregará en 2020 y el avión Mitsubishi MRJ90, programado para entrega a mediados de 2018, que exceden ambos el límite de peso.

![]() El analista Darryl Genovesi dijo que era improbable que las aerolíneas volaran el Embraer E175-E2 sólo en rutas principales, debido a mayores costos. «Esto pone en riesgo la viabilidad del E175-E2, ya que la mayor parte de la demanda se origina en las tres aerolíneas», Delta Air Lines, United Airlines y American Airlines, escribió Genovesi en una nota a los clientes.

El analista Darryl Genovesi dijo que era improbable que las aerolíneas volaran el Embraer E175-E2 sólo en rutas principales, debido a mayores costos. «Esto pone en riesgo la viabilidad del E175-E2, ya que la mayor parte de la demanda se origina en las tres aerolíneas», Delta Air Lines, United Airlines y American Airlines, escribió Genovesi en una nota a los clientes.

El operador regional SkyWest Inc, que opera vuelos para Delta, entre otros, es el cliente de lanzamiento del E175-E2, con 100 pedidos firmes. En un comunicado, Embraer dijo que su actual E-175 domina el mercado de 70 plazas, donde tiene el 84% de la cuota de mercado y el fabricante brasileño seguirá vendiendo ese avión a partir de 2020 si las cláusulas de alcance no cambian. Sin embargo, el comunicado dice: «Embraer cree que las cláusulas de alcance se relajarán en el futuro a medida que aumenten los precios de los combustibles y las aerolíneas busquen productos más eficientes».

En septiembre, la compañía Mitsubishi dijo que está trabajando con los clientes para tratar problemas de peso para el MRJ90, con un peso total de 1.323 libras, que lo convierte en un avión demasiado pesado para operaciones regionales en EEUU con la «Cláusula de Alcance», imposibilitando poder obtener un contrato con Eastern Airlines de Florida.

Bombardier contraataca

Los sindicatos de pilotos estadounidenses han tomado una línea cada vez más dura en las demandas salariales más altas y están haciendo menos concesiones a las compañías estadounidenses. Sin embargo, su posición actual en contra de las cláusulas cambiantes podría ser una bendición para la rival canadiense Bombardier Inc, que lo ve como una oportunidad para aumentar las ventas de su CRJ-900, que se ajusta a los límites de peso actuales.

El presidente ejecutivo de Mesa Air Group Inc, Jonathan Ornstein, dijo que no comprará nuevos aviones que no cumplan con las cláusulas de alcance ya que no cree que los límites actuales serán cambiados en el futuro cercano. En lugar de eso, la aerolínea regional con sede en Arizona comprará más generación actual del E-175, junto con CRJ900 adicionales para reemplazar 38 aviones regionales que se eliminarán gradualmente durante los próximos cuatro años. «No creo que haya ninguna posibilidad de que los pilotos cambien sus requisitos de peso», dijo Ornstein.

Desafortunadamente tanto para Embraer como para Mitsubishi, la mayor parte del interés en el E175 – E2 y el MRJ90 provienen de aerolíneas regionales de EE.UU., prácticamente ninguna de las cuales puede operar esos aviones sin cambios en la cláusula de alcance. Sin embargo, Embraer insiste en que el interés en el actual E175 sigue siendo fuerte en América del Norte, y Mitsubishi dice que sus grandes clientes de EE.UU. pueden optar por cambiar sus pedidos de MRJ -90s a la menor MRJ -70s, ahora programado para EIS en 2019. Mitsubishi espera entregarán el primer MRJ -90 a All Nippon Airways de Japón a mediados de 2018.

Embraer ha vendido más de 330 E175 a aerolíneas en Norteamérica desde enero de 2013, representando más del 80% de todas las órdenes en el segmento de 76 asientos, según la compañía. En tanto, Mitsubishi necesita ingresar a un mercado nuevo con su nueva aeronave regional MRJ-90, pero si la Cláusula de Alcance se mantiene, podrá ofrecer su modelo mas pequeño, el MRJ-70 para poder obstentar un jugoso contrato de las principales aerolíneas regionales de Estados Unidos. ![]()

The Scope Clauses in regional aviation

Embraer and Mitsubishi could not expand sales to the United States under the «Scope Clause» for Embraer E175-E2 and Mitsubishi MRJ-90 aircraft

The pilots of the main airlines hope to maintain the rules in force in their new work contract that prevent the US airline from flying over a certain weight on regional routes. This represents a blow to Embraer S.A. and Mitsubishi Heavy Industries Ltd., whose latest models exceed this limit, precluding sales in the US market, such as regional aircraft.

The new work contract for pilots will maintain what is known as a «Scope Clauses», which restricts aircraft over 86,000 pounds and with more than 76 seats on regional routes. The results of the vote on the new contract are expected on December 1, 2017.

The clause effectively protects well-paid pilot jobs in major airlines, as it prevents the company from using larger aircraft on regional outsourced routes, which generally pay less and have lower working conditions.

Embraer & Mitsubishi fight the US market

When Embraer and Mitsubishi’s engineers designed their latest regional aircraft, with heavier but more efficient engines, they expected the scope clause to be canceled, but the unions have managed to maintain it.

Delta’s vote will follow the similar decisions of the unions of American Airlines Group Inc. and United Continental Holdings Inc. earlier this year as in 2015. The opposition of the pilots to the scope clauses is a problem for the regional aircraft Embraer E175-E2 from Embraer to be delivered in 2020 and Mitsubishi‘s MRJ90 aircraft, scheduled for delivery in mid-2018, both exceeding the weight limit.

UBS downgraded Embraer to a «sell» rating this week. Analyst Darryl Genovesi said airlines were unlikely to fly the Embraer E175-E2 only on main routes because of higher costs. «This puts the viability of the E175-E2 at risk, since most of the demand originates from the three airlines», Delta Air Lines, United Airlines and American Airlines, Genovesi wrote in a note to customers.

Regional operator SkyWest Inc, which operates flights to Delta, among others, is the launch customer of the E175-E2, with 100 firm orders. In a statement, Embraer said that its current E-175 dominates the market for 70 seats, where it has 84% of market share and the Brazilian manufacturer will continue to sell that aircraft from 2020 if the scope clauses do not change. However, the statement said: «Embraer believes that the scope clauses will relax in the future as fuel prices rise and airlines look for more efficient products.»

In September, Mitsubishi said it is working with customers to address weight issues for the MRJ90, with a total weight of 1,323 pounds, which makes it an over-heavy aircraft for regional operations in the US with the «Scope Clauses», making it impossible to obtain a contract with Eastern Airlines of Florida.

Bombardier counterattacks

US Pilot Unions have taken an increasingly hard line in higher wage demands and are making fewer concessions to US companies. However, its current position against changing clauses could be a boon to Canadian rival Bombardier Inc, which sees it as an opportunity to boost sales of its CRJ-900, which fits current weight limits.

Mesa Air Group Inc chief executive Jonathan Ornstein said he will not buy new aircraft that do not comply with the scope clauses as he does not believe the current limits will be changed in the near future. Instead, the Arizona-based regional airline will buy more of the current generation of the E-175 along with additional CRJ900 to replace 38 regional jets that will phase out over the next four years. «I do not think there’s any chance that the drivers will change their weight requirements,» Ornstein said.

Unfortunately for both Embraer and Mitsubishi, most of the interest in the E175-E2 and the MRJ90 come from US regional airlines, virtually none of which can operate those aircraft without changes in the scope clause. However, Embraer insists that interest in the current E175 is still strong in North America, and Mitsubishi says its major US customers are. they can choose to switch their orders from MRJ-90s to the smaller MRJ-70s, now scheduled for EIS in 2019. Mitsubishi expects to deliver the first MRJ-90 to Japan’s All Nippon Airways in mid-2018.

Embraer has sold more than 330 E175 to airlines in North America since January 2013, representing more than 80% of all orders in the 76-seat segment, according to the company. Meanwhile, Mitsubishi needs to enter a new market with its new MRJ-90 regional aircraft, but if the Reach Clause is maintained, it will be able to offer its smaller model, the MRJ-70 to be able to obstruct a juicy contract of the main regional airlines of the United States. A \ W

Ξ A I R G W A Y S Ξ

SOURCE: Airgways.com

DBk: Wikimedia.org / Airgways.com

AW-POST: 201710101244AR

A\W A I R G W A Y S ®

AW | 2017 10 09 10:50 | AIRLINES MARKET

AW | 2017 10 09 10:50 | AIRLINES MARKET

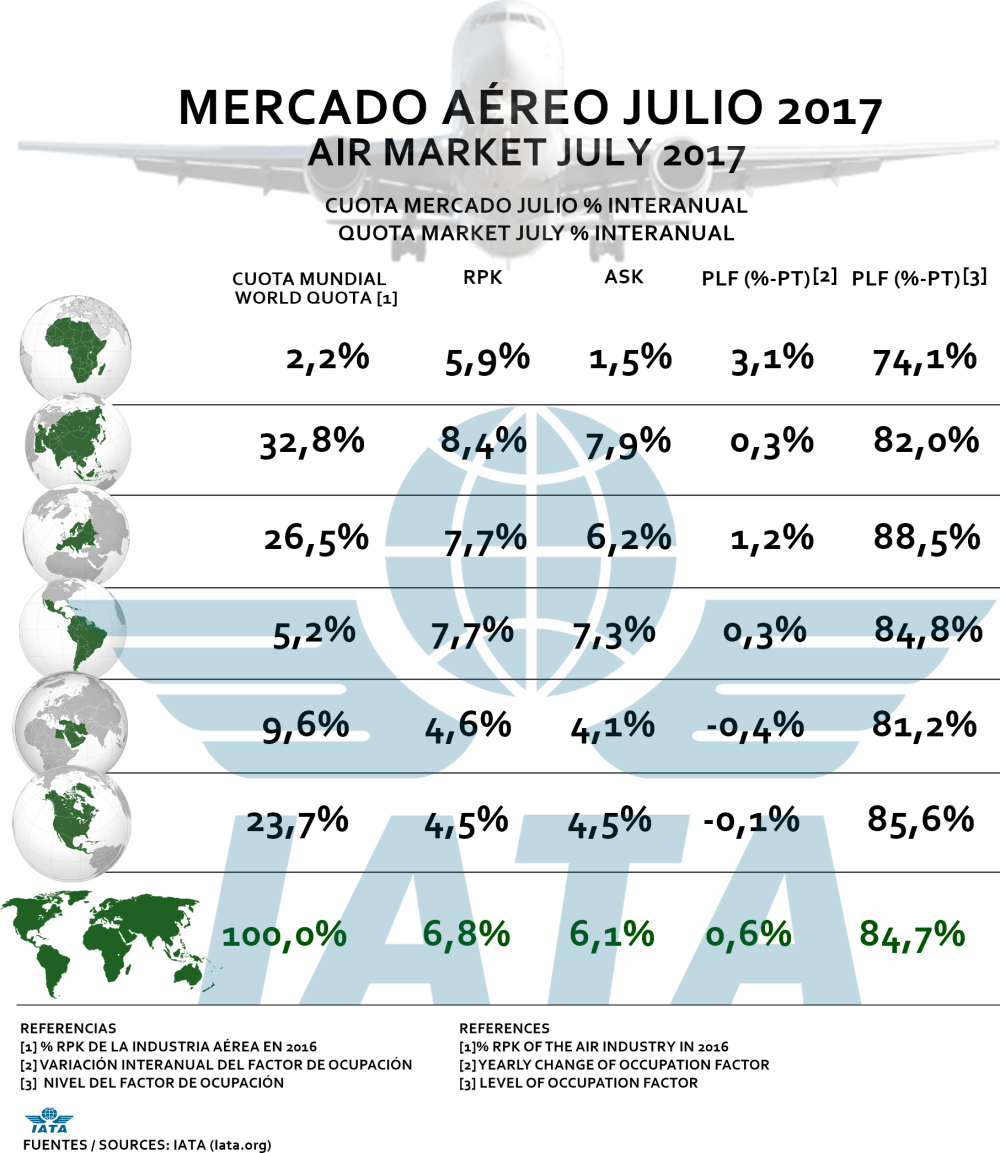

Las aerolíneas europeas experimentaron un aumento de la demanda del 7,5% interanual, frente al 8,8% de junio. La capacidad subió un 5,9% y el factor de ocupación subió 1,3 puntos porcentuales, hasta el 88,7%, el más alto respecto a las demás regiones. El contexto económico en Europa se ha fortalecido, pero los datos desestacionalizados muestran una demanda más moderada desde el pasado mes de febrero.

Las aerolíneas europeas experimentaron un aumento de la demanda del 7,5% interanual, frente al 8,8% de junio. La capacidad subió un 5,9% y el factor de ocupación subió 1,3 puntos porcentuales, hasta el 88,7%, el más alto respecto a las demás regiones. El contexto económico en Europa se ha fortalecido, pero los datos desestacionalizados muestran una demanda más moderada desde el pasado mes de febrero.