AW | 2016 10 02 18:04 | INDUSTRY

Boeing está en camino de perder su objetivo de 2016 para aviones por un amplio margen. La empresa estadounidense necesita revertir su pulseada para estar a la altura del consorcio Airbus que está dando batalla en todos sus frentes

Boeing estableció el objetivo de lograr una proporción 1 a 1 de recibir una orden para cada avión se entrega este año.

Boeing estableció el objetivo de lograr una proporción 1 a 1 de recibir una orden para cada avión se entrega este año.

A nueve meses del año 2016, las posibilidades de Boeing no se ven bien. La empresa espera entregar entre 740-745 aviones comerciales este año. Mientras tanto, a partir del martes, había reservado 357 pedidos netos en lo que va del 2016. Eso pone menos de la mitad de su objetivo de órdenes.

Sin embargo, mientras que Boeing se enfrenta a una batalla cuesta arriba para llegar a 740 pedidos, todavía tiene una oportunidad de conseguirlo.

Finalizar los acuerdos de venta recientes

En primer lugar, Boeing tiene un gran número de compromisos de aviones que todavía se están discutiendo en pedidos en firme. Por ejemplo, en Farnborough Airshow 2016, Boeing ha anunciado 182 pedidos y compromisos, pero sólo una fracción de ellos eran nuevos pedidos en firme.

Hay alrededor de 100 compromisos pendientes sobre todo para las compañías aéreas chinas que aún no se reflejan en el listado total del pedido de Boeing de 2016. Para contar los pedidos en firme, Boeing necesita finalizar los términos de la venta.

Del mismo modo, existen acuerdos históricos de Boeing para vender 80 aviones a Iran Air, todavía no ha dado lugar a ningún pedidos en firme aún. El gobierno de Estados Unidos recientemente aprobó licencias de exportación para estos aviones, pero Irán todavía tiene que alinear la financiación para cerrar el trato.

Por último, la compañía de bandera de Arabia Saudia ha anunciado recientemente planes para comprar 28 aviones de fuselaje ancho a Boeing. Al parecer, el acuerdo no es oficial todavía, ya que Boeing no ha registrado pedidos en firme de Saudia este año.

En total, Boeing tiene cerca de 200 de estas órdenes pendientes. Será difícil para Boeing finalizar todos ellos en los próximos tres meses.

Obtener pedidos esperados en el Medio Oriente

Boeing también podría estar cerca de ganar grandes pedidos a partir de las dos principales aerolíneas de Oriente Medio. Qatar Airways está a punto de ordenar al menos 30 más aviones de fuselaje ancho a Boeing, principalmente el 787 Dreamliner según la fuente periodística Bloomberg. El CEO de Qatar Airways, Akbar Al Baker ha estado disgustado con Airbus últimamente, debido a los retrasos en la entrega, por lo que la Boeing tiene poco riesgo de perder frente a Airbus.

Mientras tanto, Emirates es probable que realice un pedido de unos 70 aviones de fuselaje ancho antes de que finalice el año. Los candidatos a elegir están entre el 787 Dreamliner de Boeing y el Airbus A350. Teniendo en cuenta que Emirates ha cancelado un pedido anterior de 70 A350 en 2014, parece probable que Boeing tiene la pista despejada. También es posible que Emirates divida una orden entre Boeing y Airbus.

Capitalizar la fiebre del fin de año

Por último, Boeing tiene que tomar ventaja de la fiebre típica de fin de año para ordenar los aviones. El año pasado, Boeing terminó Q3 con sólo 447 pedidos netos. Sin embargo, se retiró en 321 pedidos netos en el Q4 de llegar a una proporción de relación de 1 entrega / 1 pedido nuevo para el año.

Boeing recibe a menudo un número desmesurado de pedidos en el cuarto trimestre. Hasta cierto punto, Boeing puede llegar a ser más agresivo hacia el final del año, ya que trata de cumplir los objetivos de ventas internas. Los ciclos de planificación de las aerolínea también pueden alentar una oleada de pedidos de fin de año. En el año 2016, es más importante que nunca para Boeing para terminar el año con una nota alta.

Boeing todavía tiene una oportunidad

Internamente, los ejecutivos de Boeing parecen reconocer que será muy difícil de satisfacer una proporción 1V/1P* este año. Boeing tendría que reafirmar los numerosos pedidos que han sido anunciados, la captura de grandes pedidos de fuselaje ancho de Emirates y Qatar Airways, y redondeando más pedidos en la carrera de fin de año.

Al final, Boeing probablemente caerá por debajo de su meta de 2016 orden. Sin embargo, los inversores todavía deben esperar ver un gran repunte en la actividad de orden en los próximos tres meses.

Airbus y Boeing podrían perder la batalla de los cielos

La campana ha sonado en otra ronda entre dos fabricantes de aeronaves dominantes del mundo. Cuando la Organización Mundial de Comercio dictaminó la semana pasada que la europea Airbus no había podido eliminar miles de millones de dólares en ayuda estatal ilegal, Boeing, su competidor trasatlántico, se apresuró a pronunciar una victoria decisiva. La realidad, sin embargo, es que muchas rondas aún están por llegar.

Sería mejor para todos si la UE y los Estados Unidos, los cuales han prodigado las diversas formas de ayuda estatal en sus industrias aeronáuticas, volvieron a la mesa de negociación, donde estaban hasta que los EE.UU. decidieron iniciar un litigio en 2006.

No sólo tiene este caso perdido demasiado tiempo y dinero. La amenaza ahora, dada la atmósfera política febril en ambos lados del Atlántico, con consecuencias más perjudiciales.

Llevado a su conclusión lógica y ninguna de las partes debe volver a bajar, esta diferencia podría dar lugar a la imposición de aranceles de represalia, y una guerra comercial que podría ser devastadora para las relaciones UE-EE.UU.

Airbus y Boeing están saliendo al mercado de aviones más pequeños

Esto permite espacio para Bombardier y Embraer para moverse en el vacío. Este vacío es de un valor aproximado de 2.000 aviones. Probablemente la mejor manera de ilustrar el punto que queremos hacer es la siguiente imagen.

Mira las grandes burbujas para el A319 y 737-700. A partir de 2Q16 había 1.430 A319 en servicio y 1.058 737-700 en servicio. Estos dos aviones casi representan el 90% de la flota mundial entre 120 y 150 asientos. Hay una pequeña flota de McDonnell Douglas retirarse rápidamente. Por lo que el mercado tiene un valor de al menos 2.500 aviones.

Las pequeñas burbujas a la derecha, se tratan de la próxima generación de los Airbus y Boeing.

Las pequeñas burbujas en la izquierda se aplican a los productos de Bombardier y Embraer. Como muestra su ubicación vertical, sus aviones son más eficientes desde el punto de vista de peso específico de la saeronaves. Sólo los aviones pueden hacer dinero de carga útil, por lo que mientras más ligero sea el avión, más eficiente es.

Tenga en cuenta el tamaño de las burbujas de la aeronave Bombardier y Embraer es mayor que para Airbus y Boeing. Airbus y Boeing han tenido que añadir asientos de sus aviones de nueva generación con el fin de escapar de la competencia, como por ejemplo la implementación de más asientos en el rediseño del B737-7 MAX. Esto ha llevado a sus nuevos modelos a subir sus capacidades operativas. Pero, al hacerlo, han abandonado el mercado de asiento por debajo de los 130 pax. Se trata de un segmento de 2.500 aviones. Es un mercado grande e importante.

Nuevos aviones para el mercado de medio rango

Dennis Muilenburg, CEO de Boeing, piensa que la empresa puede diseñar y construir dos nuevos aviones de pasajeros comerciales en un marco de tiempo que cumple con entrada prevista de su competidor Airbus en servicio, el A321NEO y roba una marcha en el razonable plan de fabricante europeo para hacer frente a la demanda de un avión para llenar el vacío entre las líneas B737 y B787, el llamado medio rango de mercado.

Un competidor para el A321NEO, que ha sido apodado como el Boeing 737-10X, podría estar listo para el mercado en 2019 o 2020, según Muilenburg. Una aeronave de este tipo es una versión alargada del Boeing 737-9 MAX con capacidad para 180 pasajeros, en una configuración de dos clases en el nuevo plano diseñado para un máximo de 198 asientos.

La empresa tiene que responder a cuatro preguntas principales antes de comprometerse a una versión alargada o más grande llamada B737-10X:

En primer lugar, si se lanza cualquier otra variante alargada, ¿será suficiente para ganar una cuota de mercado estimada del 17%? En segundo lugar, ¿será un derivado tal de mantener el valor de coincidencia familia sin dejar de ser lo suficientemente diferentes para evitar la potencial canibalización del mercado del Boeing 737-9? En tercer lugar, dependiendo del nivel de cambio, ¿podría ser la variante lanzada al mercado en el momento oportuno y ser asequible? Por último, en cuarto lugar, ¿es el mercado potencial para la variante -10x lo suficientemente importante como para merecer la interrupción que podría alterar en el sistema de cadena de producción de un nuevo derivado?

Cómo Boeing responde a estas preguntas afectarán a los planes de la compañía para un diseño de la aeronave de medio rango de acción que la compañía ha llamado a la aeronave nueva de tamaño mediano conocida como NMA que transportaría hasta 270 pasajeros en los vuelos, llegando a las 5.000 millas náuticas. La NMA se prevé que entre en servicio en torno a 2025 y depende en gran medida de la capacidad de los fabricantes de motores para desarrollar un nuevo motor con entre 40.000 y 45.000 libras de empuje.

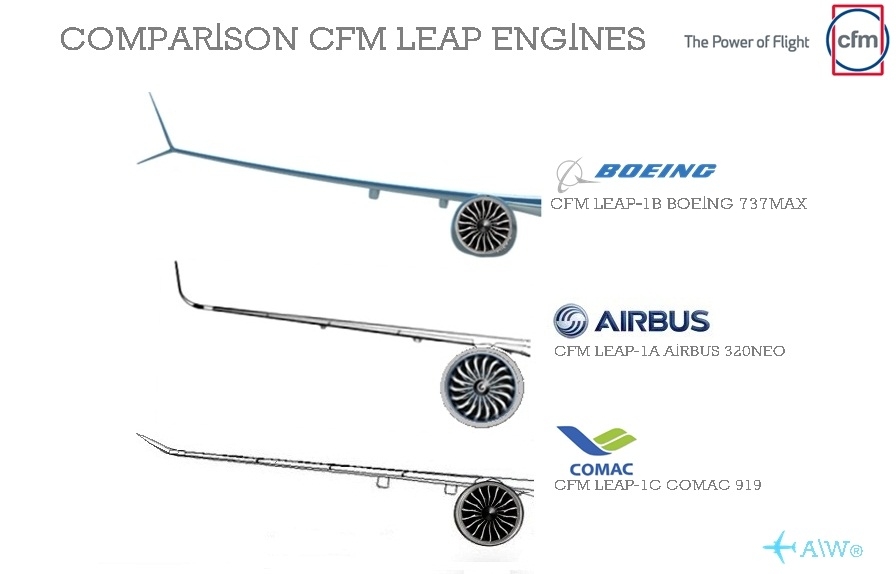

El motor CFM LEAP-1B en los aviones 737 MAX tiene una potencia de poco más de 29.000 libras de empuje de despegue, y se espera una nueva versión para elevar a 31.000. El motor LEAP-1A utilizado en el Airbus A320NEO genera 35.000 libras de empuje de despegue, y la variante LEAP-1C construido para la china Comac C919 desarrolla ya 31.000 libras de empuje de despegue. Boeing podría utilizar el más potente LEAP-1A en el 737-10X, pero eso requeriría un cambio significativo en el tren de aterrizaje del avión, al igual que la adición del LEAP-1C.

Un avión Airbus más grande, el A321LR, podía albergar hasta 240 pasajeros en vuelos de hasta 4.000 millas náuticas por simple adición de tres tanques de combustible en el espacio utilizado actualmente para equipaje y carga. El 737-10X estirado, se muestra al lado del 737-9, podría demandar $ 2 mil millones en gastos de desarrollo, un costo relativamente barato en el mundo aviones.

737-9 737-10X dibujos

Fuente: El Boeing Co .; Aviation Week

Si Boeing decide en última instancia construir dos nuevos aviones, la decisión se se tomará dependiendo del número de aviones que la compañía cree que puede vender. A principios de este mes de octubre 2016, Boeing estima la demanda de su avión NMA de 2.000 a 5.000 unidades para el mercado. Debido a que el avión sería más costoso en desarrollar, la empresa tiene que cerciorarse de que un 737-10X no canibalice el mercado antes de que el proyecto NMA esté fuera de la mesa de dibujo y en producción.

Eso podría ser más complicado que nunca, dado indicios recientes de que las compañías de bajo coste (LCC) como de Norwegian Air tienen previsto utilizar los nuevos 737-8s MAX para vuelos de larga distancia. Las nuevas aeronaves 737 MAX y A320NEO pueden volar rutas de hasta 3.200 millas náuticas en sus modelos estándar y que el A321LR añade otras 300 millas náuticas a eso.

La gran pregunta entonces para Boeing es si las aerolíneas de bajo costo impulsarán los costes de volar, por ejemplo,a Europa occidental a la costa este de los Estados Unidos, tan bajo que el mercado de un NMA se evapore. El jurado está todavía fuera de esta decisión. Los cielos son el escenario de Airbus y Boeing como los principales luchadores y donde ninguno de ellos quiere perder la batalla por los cielos.

The aerial battle for the skies of the world

Boeing is on track to miss its 2016 target aircraft by a wide margin. The US company needs to reverse its pulseada to keep up the Airbus consortium is giving battle on all fronts

Boeing set a target of achieving a 1 to 1 ratio to receive an order for each aircraft is delivered this year.

A nine months of 2016, Boeing chances do not look good. The company expects to deliver between 740-745 commercial aircraft this year. Meanwhile, as of Tuesday, there were 357 net orders booked so far in 2016. That puts less than half of its goal of orders.

However, while Boeing is facing an uphill battle to reach 740 orders, still you have a chance to get it.

Finish recent sales agreements

First, Boeing has a large number of commitments aircraft still being discussed in firm orders. For example, in Farnborough Airshow 2016, Boeing announced 182 orders and commitments, but only a fraction of them were new firm orders.

There are about 100 commitments outstanding especially for Chinese airlines that are not yet reflected in the total list of 2016 Boeing order to have firm orders, Boeing needs to finalize the terms of the sale.

Similarly, there are historical agreements to sell 80 Boeing aircraft to Iran Air, it has not yet resulted in any firm orders yet. The US government recently approved export licenses for these aircraft, but Iran has yet to line up financing to close the deal.

Finally, the flag carrier Saudia Arabia recently announced plans to buy 28 widebody Boeing. Apparently, the deal is not official yet, since Boeing has not recorded firm orders from Saudia this year.

In total, Boeing has about 200 of these outstanding orders. Boeing will be difficult to finish all of them in the next three months.

Get orders expected in the Middle East

Boeing may also be close to winning large orders from two major airlines in the Middle East. Qatar Airways is about to order at least 30 more widebody Boeing, the 787 Dreamliner mainly according to Bloomberg journalistic source. Qatar Airways CEO Akbar Al Baker has been displeased with Airbus lately, due to delays in delivery, so Boeing has little risk of losing to Airbus.

Meanwhile, Emirates is likely to make an order for 70 wide-body aircraft before the end of the year. Candidates are to choose between the Boeing 787 Dreamliner and the Airbus A350. Given that Emirates has canceled a previous order of 70 A350 in 2014, it seems likely that Boeing has a clear track. Emirates may also split an order between Boeing and Airbus.

Capitalize fever end of the year

Finally, Boeing has to take advantage of the typical year-end rush to order aircraft. Last year, Boeing ended Q3 with only 447 net orders. However, he retired in 321 net orders in Q4 to reach a ratio of 1 share of delivery / 1 new order for the year.

Boeing often receives a disproportionate number of orders in the fourth quarter. To some extent, Boeing may become more aggressive towards the end of the year, as it tries to meet the objectives of domestic sales. Planning cycles of the airline can also encourage a wave of year-end orders. In 2016, it is more important than ever for Boeing to end the year on a high note.

Boeing still has a chance

Internally, Boeing executives seem to recognize it will be very difficult to meet a 1S/1P* proportion this year. Boeing would have to reaffirm the many requests that have been announced, capturing large orders for widebody Emirates and Qatar Airways, and rounding more orders in the year-end race.

In the end, Boeing will likely fall below its 2016 target order. However, investors should still expect to see a big spike in activity order in the next three months.

Airbus and Boeing could lose both the battle of heaven

The bell has sounded in another round between two dominant aircraft manufacturers in the world. When the World Trade Organization ruled last week that the European Airbus had failed to eliminate billions of dollars in illegal state aid, Boeing, its transatlantic competitor, he hastened to utter a decisive victory. The reality, however, is that many rounds are still to come.

It would be better for everyone if the EU and the United States, which have lavished the various forms of state aid in their aviation industries, they returned to the negotiating table, where they were until the US They decided to initiate litigation in 2006.

Not only has this case lost too much time and money. The threat now, given the feverish political atmosphere on both sides of the Atlantic, with more damaging consequences.

Taken to its logical conclusion and neither party should back down, this difference may result in the imposition of retaliatory tariffs, and a trade war that could be devastating for EU-US relations.

Airbus and Boeing are coming to market smaller aircraft

This allows space for Bombardier and Embraer to move in a vacuum. This gap is approximately $ 2,000 aircraft. Probably the best way to illustrate the point we want to make is this image.

Look at the big bubbles to the A319 and 737-700. From 2Q16 there were 1,430 A319s in service and 1,058 737-700 in service. These two aircraft represent almost 90% of the world fleet between 120 and 150 seats. There is a small fleet of McDonnell Douglas withdraw quickly. So the market has a value of at least 2,500 aircraft.

Small bubbles on the right, are treated in the next generation of Airbus and Boeing.

Small bubbles on the left apply to products from Bombardier and Embraer. As shown by its vertical location, their planes are more efficient from the point of view of specific gravity of the saeronaves. Only airplanes can make money payload, so while lighter the plane, the more efficient.

Note the size of bubbles and Embraer aircraft Bombardier is higher than for Airbus and Boeing. Airbus and Boeing have had to add seats of its new generation aircraft in order to escape competition, such as the implementation of more seats in the redesign of the B737-7 MAX. This has led to new models to upload their operational capabilities. But in doing so, they have left the market below the seat 130 pax. This is a segment of 2,500 aircraft. It is a large and important market.

New aircraft for the midrange market

Dennis Muilenburg, CEO of Boeing, thinks the company can design and build two new commercial airliners in a time frame that meets planned entry of its competitor Airbus in service, the A321neo and steals a march on the reasonable plan manufacturer Europe to meet the demand for an aircraft to fill the gap between the B737 and B787 lines, called midrange market.

A competitor for the A321neo, which has been dubbed as the Boeing 737-10X, could be ready for market in 2019 or 2020, according Muilenburg. An aircraft of this type is a stretched version of the Boeing 737-9 with capacity for 180 passengers in a two-class configuration on the new plane designed for up to 198 seats.

The company has to answer four main questions before committing to a long or larger version called B737-10X:

First, if any elongated version is released, will it be enough to win an estimated market share of 17%? Secondly, is it a derivative such to maintain the value of coincidence family while still being sufficiently different to avoid potential market cannibalization Boeing 737-9? Third, depending on the level of change, it could be variant launched in a timely manner and be affordable? Finally, fourthly, is the potential market for variant -10x important enough to warrant the disruption that could alter the system of production line of a new derivative?

How Boeing answers to these questions will affect the company’s plans for a design of the aircraft mid-range of action that the company has called the new aircraft midsize known as NMA that would transport up to 270 passengers on flights, reaching 5,000 nautical miles. NMA is expected to enter service around 2025 and depends largely on the ability of engine manufacturers to develop a new engine with 40,000 to 45,000 pounds of thrust.

The CFM LEAP-1B engine 737 MAX aircraft has a capacity of just over 29,000 pounds of takeoff thrust, and a new version is expected to increase to 31,000. The LEAP-1A engine used in the Airbus A320neo generates 35,000 pounds of takeoff thrust, and LEAP-1C variant built for the Chinese Comac C919 and develops 31,000 pounds of takeoff thrust. Boeing could use the most powerful LEAP-1A in the 737-10X, but that would require a significant change in the landing gear of the aircraft, like the addition of the LEAP-1C.

A larger Airbus, the A321LR, could hold up to 240 passengers on flights up to 4,000 nautical miles by simple addition of three fuel tanks in the space currently used for baggage and cargo. The 737-10X stretched, is shown next to the 737-9, could demand $ 2 billion in development costs, a relatively cheap cost aircraft in the world.

737-10X drawings 737-9

Source: The Boeing Co;. Aviation Week

If Boeing decides to ultimately build two new aircraft, the decision will be taken depending on the number of aircraft that the company believes it can sell. Earlier this month, October 2016, Boeing estimates the demand for its aircraft NMA 2,000 to 5,000 units for the market. Because the plane would be more expensive to develop, the company has to make sure that a 737-10X not cannibalize the market before the NMA project is off the drawing board and into production.

That could be more complicated than ever, given recent indications that low cost carriers (LCC) and Norwegian Air are planning to use the new 737-8s MAX for long-haul flights. MAX 737 new aircraft and routes A320neo can fly up to 3,200 nautical miles in its standard models and that the other nautical A321LR adds 300 miles to that.

The big question then is whether Boeing LCCs fly drive costs, such as western Europe to the east coast of the United States, so low that the market for a NMA evaporate. The jury is still out on this decision. The skies are the backdrop for Airbus and Boeing as the main fighters and where none of them want to lose the battle for the skies. A\W

(*) 1V/1P: Proporción de 1 venta (1V) para recuperar por una producción (1P) 1S/1P: Proportion of 1 sale (1S) to recover production (1P)

Ξ A I R G W A Y S Ξ

SOURCE: A I R G W A Y S / fool.com / ft.com / seekingalpha.com / 247wallst.com

DBk: Photographic © A I R G W A Y S / Air Insight / CFM

AW-POST: 201610021804AR

A\W A I R G W A Y S ®

TN transmitió a las 21 hs, «El último vuelo del mensajero». El legendario Fokker F-27 de la Fuerza Aérea Argentina que ha prestado por más de 50 años servicios sociales en las remotas tierras patagónicas de Argentina.

TN transmitió a las 21 hs, «El último vuelo del mensajero». El legendario Fokker F-27 de la Fuerza Aérea Argentina que ha prestado por más de 50 años servicios sociales en las remotas tierras patagónicas de Argentina.